What Is Equity Crowdfunding? The Definitive Guide for Founders

Most founders assume raising capital means one of two things: pitching venture capitalists who want a board seat and a 10x return, or applying for a bank loan that requires collateral you don’t have yet. There’s a third path most people overlook, one that lets you raise capital through alternative business funding approaches that put your existing community at the center of the raise.

That’s equity crowdfunding. And for the right founder, it changes everything about how a capital raise works.

What Is Equity Crowdfunding?

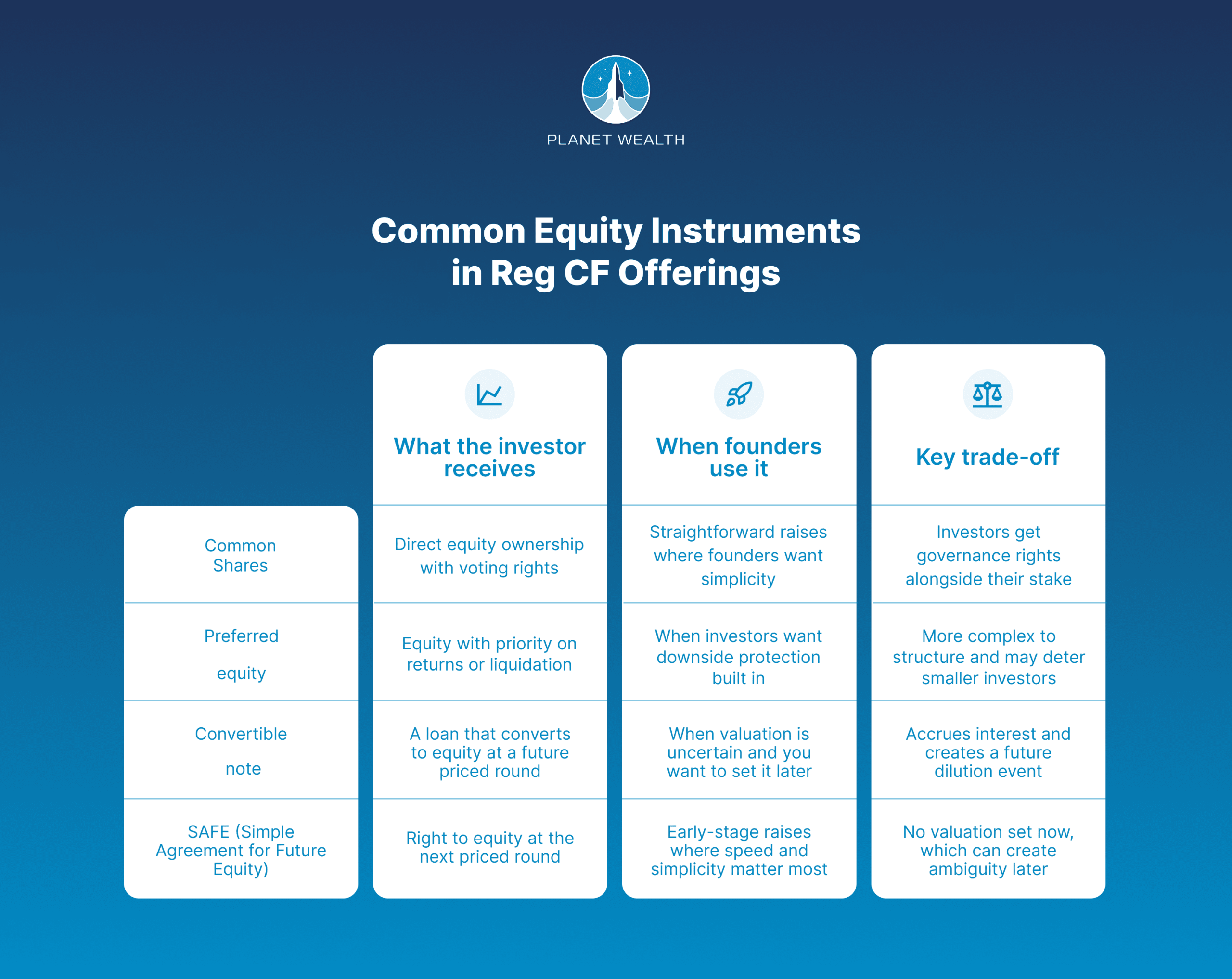

Equity crowdfunding is a method of raising capital by offering ownership stakes in your company to a large pool of investors, typically through an SEC-regulated online platform. Unlike reward-based crowdfunding, where backers receive a product or a thank-you, equity-based crowdfunding means your investors receive an actual financial stake in the business. Some people use the terms interchangeably with crowdfunding equity arrangements, where the crowd itself becomes your cap table.

This distinction matters. When someone invests in your equity crowdfunding campaign, they’re not donating and they’re not pre-ordering. They’re becoming part owners. Their return depends on how your business performs.

That’s a meaningful commitment on both sides, which is why the process is governed by federal securities law;it’s not just a campaign page and a payment processor. The legal foundation came from the Jumpstart Our Business Startups (JOBS) Act, signed into law on April 5, 2012, the legislation that opened private company investment to everyday Americans for the first time in nearly 80 years.

The Regulatory Framework: Three Paths, One Decision

Equity crowdfunding isn’t a single instrument. It operates under three different SEC frameworks, each with its own raise limits, investor eligibility rules, and disclosure requirements. Understanding the difference is the first thing any founder should do before deciding to raise this way.

| Framework | Raise limit | Who can invest | Complexity |

| Reg CF (Regulation Crowdfunding) | Up to $5M per 12 months | Accredited and non-accredited investors | Low to moderate |

| Reg A (Regulation A+) | Up to $75M | General public | Moderate to high |

| Reg D | No cap | Accredited investors only | Moderate |

Regulation Crowdfunding (Reg CF) is the framework most founders start with. Reg CF is an SEC exemption that allows companies to raise up to $5 million in a 12-month period from both accredited and non-accredited investors through a FINRA-registered funding portal. The raise must be conducted through an approved portal, like Planet Wealth, a platform authorized to facilitate these transactions.

Reg CF is designed to be accessible: your investors don’t need to meet income or net worth thresholds to participate, which means your actual customer base can invest. Before committing to a Reg CF raise, it’s worth understanding the pros and cons of a Reg CF raise in full.

Regulation A (Reg A+) raises the ceiling significantly, up to $75 million, but requires more disclosure and a longer timeline. You’ll file an offering circular with the SEC and go through a qualification process before your campaign can open. Reg A is better suited for companies that need to raise beyond Reg CF’s limit and have the resources to manage a more involved process.

Regulation D (Reg D) is a private placement exemption that covers the SEC exemption most founders overlook, primarily used to raise from accredited investors: individuals who meet specific income or net worth thresholds defined by the SEC. There’s no investor cap under Reg D, but your pool is limited to qualified individuals. This is the framework behind most traditional angel and VC rounds.

Not every company qualifies for Reg CF. The SEC disqualifies certain issuers from using this exemption, including non-US companies, companies already filing public reports under the Exchange Act, and those with prior securities law violations. The SEC’s Regulation Crowdfunding guidance has the full eligibility criteria.

Reg CF vs. Reg A: which one applies to your raise?

If you’re raising under $5 million and want to open your round to everyday investors including your customers, Reg CF is almost certainly the right starting point. If you’re planning a larger round and have the infrastructure to support the disclosure requirements, Reg A is worth a serious look. The two frameworks are not mutually exclusive over time: many companies start with a Reg CF raise and graduate to Reg A as they scale.

Who Can Invest in a Reg CF Raise?

One of the most important things Reg CF changed is who gets to participate in early-stage investing. Before the JOBS Act made regulation crowdfunding possible in 2016, private fundraising rounds were largely restricted to accredited investors.

An accredited investor is an individual who meets specific income or net worth thresholds set by the SEC: generally $200,000 in annual income or $1 million in net worth, excluding a primary residence. Before Reg CF, that qualification was essentially the entry ticket to private company investment.

Reg CF broke that open. Under this framework, non-accredited investors can participate, though their investment amounts are capped on a per-year basis across all Reg CF offerings.

According to the SEC’s current Reg CF guidance, investors whose annual income or net worth is below $124,000 can invest the greater of $2,200 or 5% of whichever figure is lower. Those with both income and net worth above $124,000 can invest up to 10% of their income or net worth, capped at $124,000 in any 12-month period.

For the exact figures on how investment caps work under Reg CF, including how the limits apply when you have multiple investments across different platforms, the rules are more straightforward than most founders expect. Accredited investors face no such limit on individual investment size within the offering.

The practical implication for founders: your raise is open to your customers, your community, and anyone who follows what you’re building, not just high-net-worth individuals with an existing relationship to private markets.

One thing to know about liquidity: securities purchased through a Reg CF offering are generally restricted from resale for one year following the close of the offering, as established under the SEC’s Regulation Crowdfunding rules. Investors should factor this into their decision, and founders should communicate it clearly during the raise.

Equity Crowdfunding vs. Other Fundraising Paths

Choosing how to raise capital is never just about the money. It’s about the terms, the relationships, and what you’re committing to on the other side of the transaction.

Venture capital offers larger checks and operational support, but it often comes with dilutive terms, board representation, and an expectation of venture-scale returns. If your business isn’t on a path to a $100M+ exit, many VC funds won’t be a fit regardless of how strong the company is.

Angel investors can be more flexible, but finding them requires warm introductions and navigating a network that isn’t equally accessible to every founder. Check sizes vary widely and the process can take months without any guarantee of closing.

Bank loans and SBA financing don’t dilute your equity, but they require collateral, personal guarantees, and a revenue history that many early-stage companies don’t have.

Reward-based crowdfunding (Kickstarter, Indiegogo) is excellent for product validation and presales but doesn’t put capital on your balance sheet the same way. You’re building a customer list, not an investor base.

Equity crowdfunding sits in a different position than all of these. You raise from people who believe in the business, you set your own terms, and you maintain control without negotiating against someone who does this professionally. The trade-off is real: you’ll have more investors to communicate with, the raise requires genuine marketing effort, and SEC compliance is not optional. The founders who run successful community raises treat the campaign itself as a strategic event, not just a capital-raising exercise.

The Community Raise Momentum Loop

Here’s what makes equity crowdfunding structurally different from a private placement with a handful of angels: when your investors are also your customers, the raise compounds in ways a traditional round doesn’t. How the community raise model works in practice goes deeper on the mechanics behind this.

An investor who already uses your product tells their network about the campaign. Their network invests. Some of them become customers. Your investors have a financial reason to refer business to you, write reviews, and advocate for the brand, because your success is now their success too.

The momentum behind this model is real. Since Reg CF went live in May 2016 through the end of 2024, the SEC reports that issuers have raised over $1.3 billion across approximately 3,800 offerings. The majority of them are small, early-stage companies with median assets under $100,000 at the time of their raise. These aren’t companies with institutional backing and venture networks. They’re companies with communities.

For founders in categories with loyal customer bases, including food and beverage brands, mission-driven SaaS and tech founders, and energy companies with community stakeholders, this flywheel effect is often more valuable than the capital itself.

How Does Equity Crowdfunding Work? The Reg CF Process Step by Step

Understanding how crowdfunding works in a regulated context is different from launching a Kickstarter. A Reg CF offering has specific mechanics every founder should know before starting.

- Choose a FINRA-registered funding portal. Your raise must be conducted through a portal registered with the SEC and FINRA. This is a mandatory requirement under Reg CF. When evaluating portals, look at their compliance infrastructure, investor reach, campaign support, and fee structure. FINRA’s funding portal directory lists all registered portals currently authorized to facilitate Reg CF offerings.

- File Form C with the SEC. Before your campaign goes live, you’ll submit a disclosure document covering your financials, use of proceeds, ownership structure, and offering terms with the SEC’s EDGAR system. Founders who prepare this early save significant time later.

Disclosure requirements by raise amount under Reg CF

| Raise amount | Financial disclosure required |

| Up to $124,000 | Internally prepared financial statements, with CEO certification |

| $124,001 to $618,000 | Reviewed financial statements from an independent CPA |

| $618,001 to $5,000,000 | Audited financial statements (first-time issuers may use reviewed statements for their initial raise) |

Source: SEC Regulation Crowdfunding guidance

- Launch and run the campaign. Once the offering period opens, investors can review your campaign and commit funds through the portal. Any material question asked by a prospective investor must be answered publicly, so all potential investors can see it. Understanding what makes a Reg CF campaign work and how to market your raise compliantly is worth studying before you open the offering period.

- Close the round and issue securities. After the raise closes, you’ll issue securities to investors per your offering terms and file a closing Form C with the SEC. Note that securities issued under Reg CF carry a one-year resale restriction for investors.

- Fulfill ongoing reporting requirements. Reg CF issuers are required to file annual reports with the SEC for as long as they have more than 300 investors of record, or until they complete a larger registered offering. How to manage investor communications after your raise is a practical guide to what that looks like on an ongoing basis.

Founders who are prepared, with financials in order, a clear narrative, and a community ready to activate, typically run campaigns over 90 to 180 days from opening to close.

Is Equity Crowdfunding Right for Your Raise?

Equity crowdfunding works best for founders who have something to activate: an existing customer base, an engaged email list, a social following, or a community of people already bought into what you’re building. The raise surfaces that belief and gives it somewhere to go.

It’s worth being honest about the other side. If you’re pre-product with no audience yet, equity crowdfunding is a harder starting point–not impossible, but the marketing lift is significant without an existing base to activate.

If your business is in a sector that benefits from stealth, where public disclosure of your financials and business plan could create competitive risk, Reg CF’s mandatory transparency requirements may be a constraint worth weighing carefully. And if a raise doesn’t hit its target, it helps to know what to do if your campaign falls short before you start, not after.

But if you have a business people already care about, a story worth telling, and a community that would jump at the chance to own a piece of what you’ve built, a community-powered raise through Reg CF is worth a serious look. See if your industry is a fit if you’re outside the categories above.

Planet Wealth is built to give founders the infrastructure to run that raise themselves. Explore Planet Wealth’s fundraising platform.