How to Raise Capital Without VCs in 2026

In 2021, U.S. venture capital hit its highest point on record: $358.2 billion invested across 19,634 deals, according to PitchBook and the NVCA. By 2023, deal value had fallen to $168.8 billion. Deal count in 2024 was still roughly 22% below that peak. And the partial recovery that appeared in 2025 was almost entirely a function of AI investment, which absorbed nearly half of all U.S. VC deal value in Q4 of that year.

For founders outside that narrow lane, the funding market that existed in 2021 is gone. The founders who are adjusting fastest are the ones who stopped treating that as a temporary condition and started treating it as the baseline.

So here’s what VC looks like for non-AI businesses in 2026, what the real alternatives are and how each one works mechanically, and where equity crowdfunding fits in the picture.

The VC Market in 2026 Is Not the One Founders Were Sold On

Venture capital is recovering, but not evenly, and not in ways that reach most founders.

The 2021 market was a specific product of a specific moment. Zero interest rate policy (ZIRP) pushed institutional capital toward riskier asset classes. VC funds raised record amounts, deal pace accelerated, and valuations inflated at every stage from pre-seed through growth.

That environment produced expectations: faster diligence, higher pre-money valuations, and more capital deployed earlier. None of those conditions exist today.

The correction has been structural, not cyclical. Fund managers who raised during the ZIRP era have been unable to generate the returns required to raise follow-on funds. In 2024, 30 firms accounted for more than 68% of all U.S. VC fundraising.

Capital is concentrating in fewer, larger, more established hands, and those hands are deploying it selectively. The NVCA estimates $307.8 billion in dry powder available as of 2024. Investors are holding it.

Two numbers tell the stage-level story clearly: First, 30% of all VC deals in 2024 involved flat or down rounds. Second, median deal values continued declining from their 2021 peak across every stage of funding. There is capital in the system. It is not reaching early-stage founders at 2021 terms, and it is not reaching them at 2021 volume.

Geography compounds the problem. VC deal flow remains concentrated in places like California, New York, and Massachusetts. The median fund size outside those three states was $10 million in 2024, per NVCA data, versus a national median of $21.3 million.

A founder in Texas, Tennessee, or anywhere without a dense institutional network is not just competing for fewer dollars. They are operating in a structurally different market.

Why Chasing VC Is the Wrong Default for Most Founders

The Ladder Was Never as Open as It Looked

Venture capital has always been a narrow path. The pitch circuit obscures that fact. The shared language of “seed rounds” and “Series A” implies a structured ladder that any founder with a strong business can climb. That ladder was never as broadly available as the ecosystem suggested. It is narrower now.

The Return Math Most Founders Don’t Fit

VC firms target fund-level returns that require individual investments to return 10 times the capital or more. That math only works in markets large enough to support exits at a scale that moves the needle for a $100 million or $500 million fund. A profitable F&B brand, a regional energy company, or a vertical SaaS business serving a defined market may be an excellent business. It may not be a VC-fundable one, and that distinction matters before a founder spends a year finding out.

What Dilution Actually Costs You

Here’s how a typical three-round raise plays out on the cap table:

| Round | Cap | Founder Ownership Remaining |

|---|---|---|

| Pre-seed | $4 million | ~85 to 90% |

| Seed | $10 million | ~65 to 70% |

| Series A | $20 million | Below 50% |

That ownership erosion happens before most founders reach product-market fit. Liquidation preferences compound it further. They are standard in institutional deals and mean investors recover their capital first in any exit. A founder who sells their company for $15 million after raising $12 million on those terms can end up with very little, or nothing, once preferences are applied.

Related reading: Equity Crowdfunding vs. Venture Capital: What Founders Actually Give Up With Each

The Time Cost Nobody Puts on the Cap Table

A serious VC raise takes months, and most of it doesn’t show up in a pitch deck:

- Building the target list

- Managing warm introductions

- Preparing data room materials

- Running follow-up

- Absorbing passes, which is most of what actually happens

For a founder who needs to be operating the business, that is not a free activity.

So Who Is VC Actually For

None of this is an argument against VC as a category. It is an argument that VC fits a specific profile, and most founders do not match it. Founders who understand the fit criteria clearly, including market size, return profile, geographic access, and ownership trajectory, can make a rational decision. Founders who treat VC as the default because it is the most visible option tend to find out the hard way.

How Founders Are Actually Raising Capital in 2026

The alternatives to VC are not new. What has changed is that more founders are using them as primary strategies rather than fallback plans. Here is how each path works.

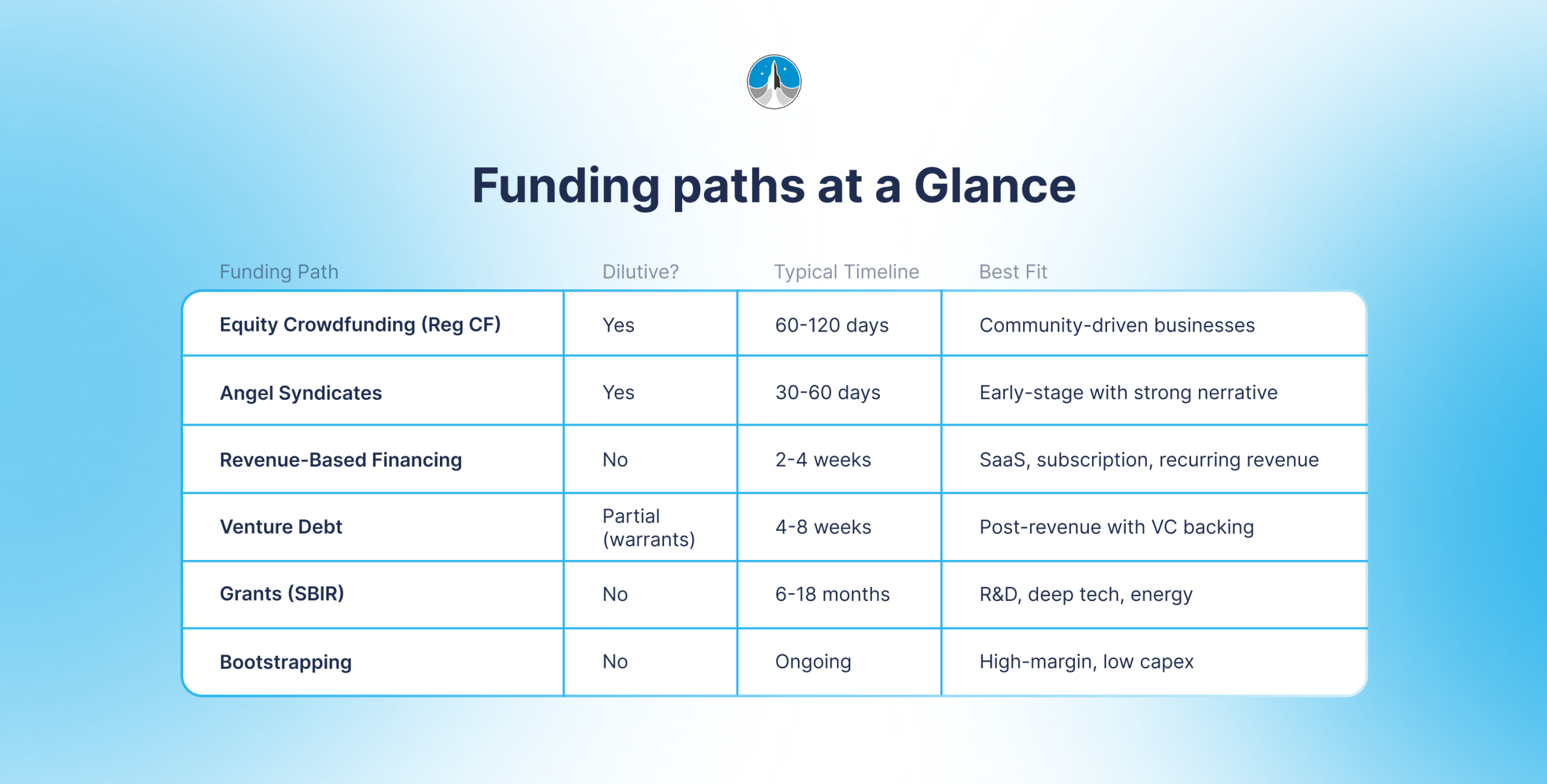

Equity Crowdfunding (Reg CF)

Regulation CF allows U.S. companies to raise up to $5 million from the general public, including non-accredited investors, through a registered funding portal. The $5 million ceiling was set by the SEC’s 2021 amendments to Reg CF, up from the original $1.07 million cap that had constrained most campaigns since the JOBS Act of 2012.

The mechanics are specific. A campaign runs through a single registered portal. The company sets a target raise and a maximum. Investors, who can include customers, community members, and retail participants, commit over a defined window, typically 60 to 90 days. When the minimum is met, funds are released. If it is not, commitments are returned.

The investor base is what separates equity crowdfunding from every other startup funding path. Instead of one or two institutional gatekeepers deciding whether the business fits their mandate, a Reg CF campaign distributes that decision across hundreds or thousands of people who already have some connection to the product, the mission, or the industry.

The community dynamic has downstream value beyond the capital itself. Investors in a Reg CF campaign are not passive. They have a financial stake in the outcome. They refer customers, share content, provide product feedback, and advocate for the business in ways that institutional investors generally do not. For consumer-facing founders, that flywheel compounds over time.

What equity crowdfunding requires in return is real marketing capability. A Reg CF campaign does not close itself. Founders who run successful campaigns treat the raise like a product launch: audience building before the campaign opens, email capture, community activation, and consistent communication throughout the raise window. Founders who approach it passively tend not to hit their minimums.

Related reading: Behind the Funnel: What Successful Reg CF Campaigns Get Right

Angel Syndicates

Angel syndicates pool capital from multiple individual investors under a lead who manages deal terms and coordinates the group. Check sizes are larger than an individual angel can write, diligence is lighter than institutional VC, and timelines are shorter, often 30 to 60 days from first conversation to close.

The practical limitation is access. Getting in front of a quality syndicate lead typically requires a warm introduction or an existing relationship. Platforms have made syndicates more discoverable, but the best deal flow still moves through networks. For founders without those connections, this path is harder to activate from a standing start.

Carry and management fee terms vary by syndicate lead and are negotiable. Valuations are less formulaic than at the institutional level, which can work in a founder’s favor when the business does not fit a standard VC template.

Revenue-Based Financing

Revenue-based financing is non-dilutive capital repaid as a fixed percentage of monthly revenue until a multiple of the original amount is returned. No equity changes hands. No board seats are involved. The repayment schedule adjusts with revenue: a slow month produces a smaller payment, a strong month produces a larger one.

This works for businesses with predictable recurring revenue, primarily SaaS companies, subscription models, and e-commerce operations with consistent monthly volume. Providers underwrite against revenue history and growth trajectory. The cost of capital is typically higher than a bank loan: traditional bank term loans average roughly 7% to 8% APR in 2026, while revenue-based financing, converted to an annualized rate, typically runs 10% to 25% for well-qualified SaaS borrowers and can reach 75% for faster repayment or higher-risk profiles.

For founders who have a realistic view of their equity’s future value, paying that premium to avoid dilution is often rational.

Venture Debt

Venture debt is loan capital extended to companies that already have institutional backing. It is dilution-light because lenders take warrants rather than equity, but it is not dilution-free. Lenders generally require existing institutional backing or strong revenue metrics to qualify.

The most common use case is runway extension: a company closes a Series A, draws venture debt to extend its cash position without giving up additional equity, and uses the runway to reach the next milestone on stronger terms. Founders without existing VC relationships will generally not qualify for this path.

Grants (SBIR and Others)

SBIR grants are federal non-dilutive funding for small businesses doing R&D in areas prioritized by federal agencies. They are worth pursuing for energy founders and deep tech companies because the capital is non-dilutive and the amounts can be material. The application and award cycle typically runs six to 18 months. SBIR belongs in the picture as a parallel track, not a primary path.

Bootstrapping

Bootstrapping is the practice of building and growing a business using personal savings, revenue from sales, or other resources you already control, rather than relying on outside funding like venture capital or loans.

Bootstrapping works for some businesses and is not viable for others. Capital-intensive operations, including food production, hardware, and energy infrastructure, cannot realistically bootstrap to scale. High-margin software or services businesses sometimes can.

A bootstrapped founder who reaches $2 million in ARR owns all of it. A funded founder who gets there faster owns a fraction. Which is better depends entirely on what the business requires and what the founder is building toward.

Why Equity Crowdfunding Is Gaining Ground

Reg CF has a structural advantage that gets more valuable in a selective VC market: the raise does not depend on a small number of institutional decision-makers agreeing to fund it.

A traditional seed round lives or dies on whether two or three partners at the right firms think the business fits their mandate. A Reg CF campaign distributes that decision across hundreds or thousands of people, many of whom are already close to the product, the category, or the mission. When VC capital is concentrated in AI and held by 30 firms managing 68% of the fundraising volume, that distribution looks like access.

The model is also structurally well-suited to the three categories where conventional VC fit has always been weakest. F&B founders have customer bases that can become investor bases. Energy entrepreneurs often have a mission-driven community that translates directly to campaign engagement. SaaS founders with a defined user base can activate that base in ways that institutional fundraising cannot replicate.

Equity crowdfunding is not right for every business. It requires marketing capability, an existing or buildable audience, and a product or mission that translates to public investors. Founders who have those things are operating in a 2026 funding climate where equity crowdfunding’s relative value has gone up, precisely because the alternatives have narrowed.

Related reading: Why 2026 Is the Best Year for Raising Through Equity Crowdfunding

What a Successful Capital Raise Actually Requires

Regardless of the path, three things determine whether a raise succeeds: a defensible number, prepared materials, and sequencing.

A defensible number means knowing exactly how much capital the business needs, what milestone it funds, and how the money gets deployed line by line. Investors across every path will probe this. A founder who cannot answer it precisely signals that the raise is not ready.

Prepared materials means the core documents exist before the raise opens: financial model, investor deck, use of funds summary, and in the case of Reg CF, the Form C filing. Starting a raise and building materials in parallel is a common and costly mistake.

Sequencing means running the right tracks at the right time. A founder pursuing Reg CF and SBIR simultaneously is not overextended. They are running a faster path in parallel with a longer one, which is rational given SBIR’s 6 to 18-month cycle. A founder waiting for a single VC to respond before exploring alternatives is placing a single bet in a market that does not reward passivity.

Which capital you take, from whom, at what terms, shapes who has a say in the company five years from now. That decision deserves more deliberation than most founders give it.

FAQ

How do you raise capital for a startup?

The viable paths depend on stage. Pre-revenue startups have fewer options: angel syndicates, SBIR grants, and equity crowdfunding are the most accessible. Post-revenue businesses can add revenue-based financing and venture debt. The right starting point is matching the path to the business’s actual profile, not to which option carries the most perceived status.

How do you raise capital for a business?

The first question is whether you want dilutive or non-dilutive capital. Equity fundraising through VC, angel syndicates, or equity crowdfunding gives up ownership in exchange for capital with no fixed repayment schedule. Revenue-based financing and grants do not dilute ownership but require existing revenue or a qualifying R&D focus. Most businesses have a clearer answer to that question than founders initially assume.

How do you raise venture capital?

VC fits businesses with a large addressable market, typically $1 billion or more, a realistic path to a 10x or better return for the investor, and warm network access to active deal flow. If those criteria fit, the path is introductions to relevant partners, a clear deck, and a precise answer to why this business returns the fund. If they do not fit, the time spent in that process has an opportunity cost that compounds.

How do you fund a startup with limited resources?

Equity crowdfunding, SBIR grants, and angel syndicates are the most accessible options for early-stage businesses without significant revenue. Reg CF allows founders to raise up to $5 million from a broad investor base, including customers and community members, without the institutional network that VC requires. The trade-off is marketing effort. There is no version of a successful Reg CF campaign that runs on autopilot.

How do you raise money for a business without taking on debt?

Equity-based options, including Reg CF, angel syndicates, and VC, and non-dilutive options, including revenue-based financing and SBIR grants, both operate outside traditional bank financing. Equity capital does not require repayment on a fixed schedule but costs ownership. Revenue-based financing requires repayment from revenue but preserves equity. The choice comes down to which asset matters more to protect.

Related reading: The Pros and Cons of Regulation Crowdfunding

Founders who built their raise strategy around VC in 2021 are not operating in the same market. The deal count is lower, the capital is more concentrated, and the AI-driven recovery has largely bypassed the sectors where most founders are building. The funding paths that have matured in response, equity crowdfunding in particular, are not consolation prizes. They are the primary option for founders who match the model.

If you want to understand where your raise stands, get in touch with the Planet Wealth team.