Reg A+ Explained: The Mini-IPO That Lets Companies Raise Up to $75M from the Public

Most founders operating outside the VC system eventually run into the same ceiling: equity crowdfunding under Reg CF caps out at $5 million, and a traditional IPO costs more and takes longer than most growth-stage companies can absorb. Between those two extremes sits a structure that most founders never seriously evaluate: Regulation A+.

Reg A+ is an SEC registration exemption that allows eligible companies to raise up to $75 million per year from both accredited and non-accredited investors, without a full S-1 registration.

Reg A+ is often compared to a mini-IPO. The raise is public, the investor pool is open, and the SEC reviews your offering statement before it goes live. It’s still not a full listing though. Your securities do not automatically trade on a public exchange when the raise closes.

This post covers the mechanics, the two tiers, the eligibility requirements, and the real cost picture, so you can evaluate whether Reg A+ belongs in your capital strategy.

What Is Reg A+?

Regulation A+ was enacted under Title IV of the JOBS Act in 2012 and updated by the SEC in 2015. It allows eligible companies to offer and sell securities to the general public without registering under a full S-1, which is the standard IPO process.

What makes Reg A+ structurally different from most exempt offerings is the combination of raise ceiling and investor access. Reg D’s most-used path (506(c)) is effectively limited to accredited investors.

A Reg A+ offering can be marketed to and purchased by any retail investor in the US. The capital ceiling is meaningfully higher than Reg CF. Those two features together explain why the mini-IPO comparison holds.

One point worth stating plainly for any investor-facing materials you produce: SEC qualification of a Reg A+ offering is not an endorsement of the company or the securities. The SEC reviewed your disclosure. That is not the same as approving the investment. The distinction is legally and reputationally significant.

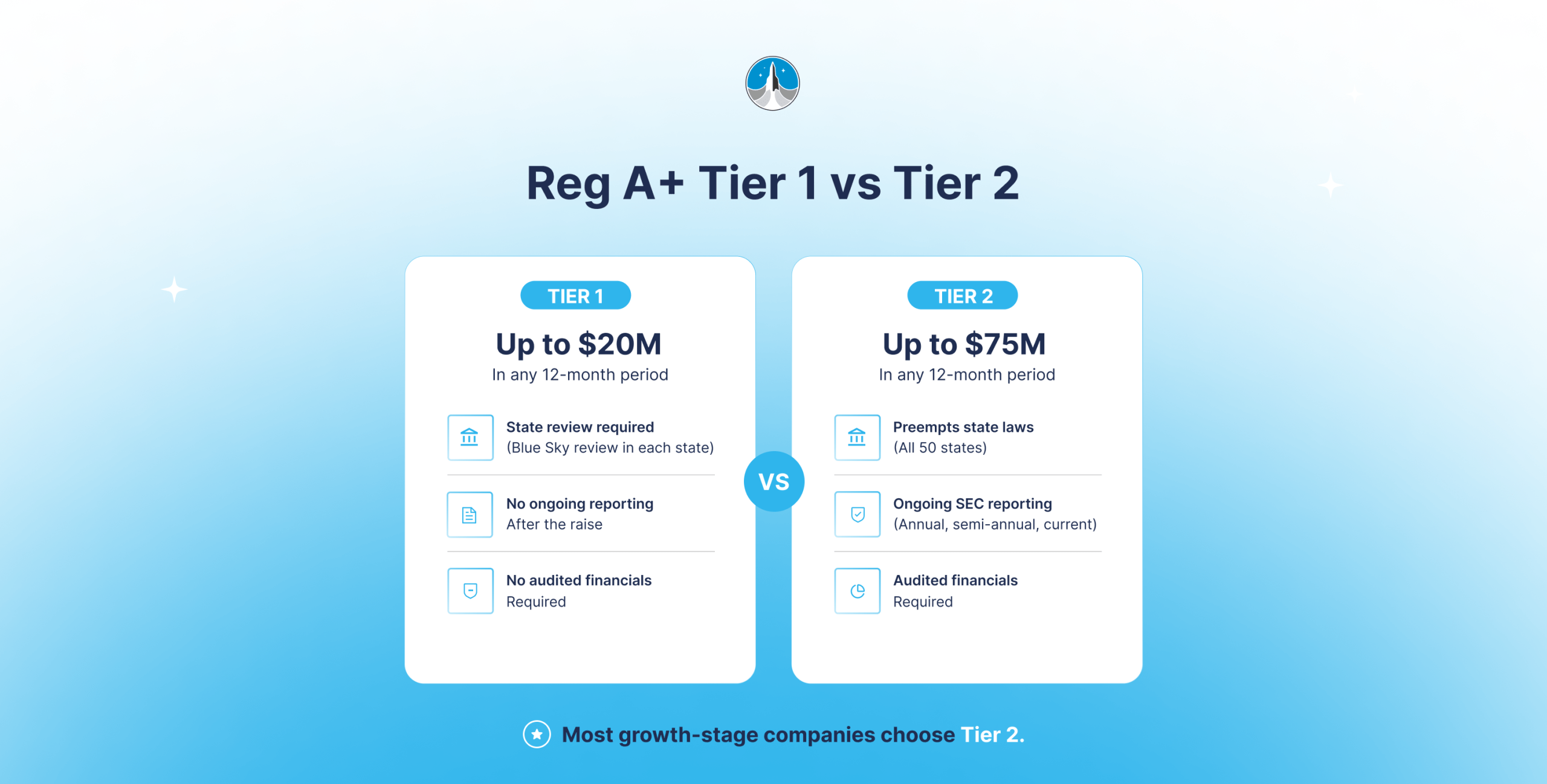

Reg A+ Tier 1 vs. Tier 2: Which One Do You Actually Need?

The regulation divides into two tiers with different raise limits, compliance requirements, and regulatory treatment. Here’s a detailed comparison:

| Tier 1 | Tier 2 | |

| Raise limit | $20M per 12-month period | $75M per 12-month period |

| State review | Required in each state where you sell (coordinated Blue Sky review) | Preempted; file once with the SEC and sell across all 50 states |

| Financial statements | Not required to be audited | Audited financials required from an independent accountant |

| Ongoing reporting | Exit report to SEC only; no ongoing obligations | Annual report, semi-annual report, and current report for material events |

For most founders, Tier 2 is the right answer. Coordinating Blue Sky review across multiple states is expensive, slow, and operationally complex. The $20 million Tier 1 ceiling combined with that compliance overhead usually makes Tier 1 the harder path, not the easier one.

Tier 2 costs more upfront in audit and filing fees, but the federal preemption is worth it once you account for what state-by-state review actually takes.

The ongoing reporting requirements under Tier 2 are real obligations, not formalities. Build them into your operational budget before committing to the structure.

Who Can Raise Using Reg A+?

Eligibility is restricted to companies that are organized and operating in the United States or Canada, not already subject to SEC reporting requirements, and not a blank check company, investment company, or issuer of fractional undivided interests in oil or gas rights. That last category excludes certain real estate structures and pooled investment vehicles.

The clearest fit is a growth-stage company with demonstrated traction: a real product, some operating history, and a capital need between $5 million and $75 million that is too large for Reg CF and too early, too small, or too costly for a traditional IPO.

Pre-revenue companies are not technically excluded, but Tier 2 requires audited financials, and the SEC qualification process involves meaningful scrutiny. A company with no operating history and nothing to audit will face a materially harder path.

Who Can Invest?

This is the structural advantage that separates Reg A+ from most other exempt offering frameworks. Both accredited and non-accredited investors can participate.

Under Tier 2, non-accredited investors are subject to an investment cap: no more than 10% of the greater of their annual income or net worth per 12-month period. Accredited investors face no cap.

What this opens up in practice is a genuinely broad investor base. You are not limited to angels, family offices, and institutions. You can raise from customers, community members, employees, and retail investors who believe in what you are building but have never had access to early-stage company ownership.

For consumer-facing brands or mission-driven companies with an existing following, that is a real structural advantage. It can also function as a brand-building exercise, converting supporters into shareholders with a financial stake in the outcome.

Community-aligned capital is not the right fit for every raise. But if your business has an existing audience with genuine conviction, Reg A+ lets you monetize that relationship in a way that institutional capital structurally cannot.

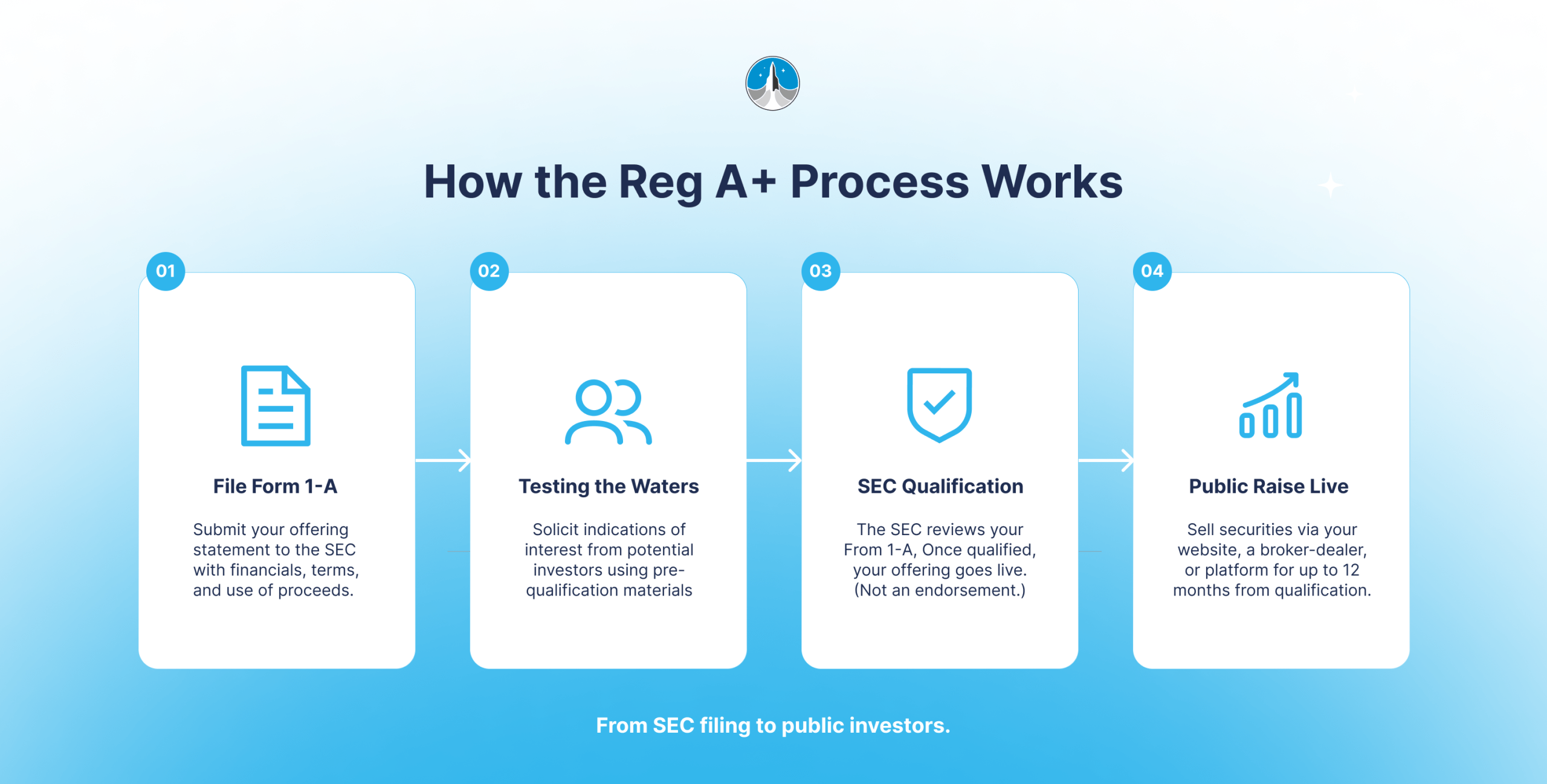

How the Reg A+ Process Works

The process follows a defined sequence.

File Form 1-A with the SEC. This is the offering statement, the Reg A+ equivalent of an S-1. It includes a description of the company and its business, the offering terms, the intended use of proceeds, and the financial statements. For Tier 2, those financials must be audited.

Testing the waters. Before the SEC qualifies your offering statement, you can solicit indications of interest from potential investors using pre-qualification materials. This is called testing the waters. It lets you gauge demand and build your investor list before the offering is formally live. Specific rules govern what those materials can and cannot say.

SEC qualification. The SEC reviews your Form 1-A and may issue comment letters requiring clarification or additional disclosure. Once qualified, the offering is live. Qualification is not an endorsement.

The raise. Once qualified, you can sell securities through your own website, a registered broker-dealer, or a third-party platform. The $75M limit applies per rolling 12-month period; offerings can run continuously beyond a year with required annual updates.

Post-raise reporting. Under Tier 2, annual reports (Form 1-K), semi-annual reports (Form 1-SA), and current reports for material events (Form 1-U) are required on an ongoing basis until you either complete a full SEC registration or meet the conditions for exiting the reporting obligation.

Related reading: Marketing Your Raise the Compliant Way: The Dos and Don’ts for Ads

What Does a Reg A+ Offering Actually Cost?

More than most founders expect, and less than a traditional IPO. The honest range for smaller raises is $50,000 to $100,000 in total offering costs, with legal fees representing the largest single line item.

For Tier 2 raises approaching the $75 million ceiling, total costs can run significantly higher once you account for audit fees, broker-dealer commissions, and ongoing compliance overhead.

Breaking it down by category:

- Legal fees cover drafting and filing the Form 1-A, responding to SEC comments, and advising on offering terms. This is not a document you can template your way through. Budget for experienced securities counsel.

- Audit fees are required for Tier 2. If your company has not previously had audited financials, getting your books to audit-ready standards takes time and cost before you can even engage the auditor.

- Broker-dealer fees apply if you use a registered broker-dealer to run the offering. Commission structures vary.

- Platform fees apply if you raise through a third-party platform. Platforms typically charge a percentage of capital raised plus ongoing compliance support.

- Ongoing reporting is an operating cost that does not end when the raise closes. Factor in accounting, legal review, and filing costs for annual and semi-annual reports.

Reg A+ is not appropriate for founders who need capital in 90 days or who are operating without room for pre-raise expenditure. The preparation window from decision to qualified offering typically runs several months.

If the timeline or cost structure does not fit your current situation, Reg CF or a Reg D offering may be more appropriate depending on how much you need to raise and who you want to raise from.

Reg A+ vs. Reg CF: How Do the Two Compare?

| Reg CF | Reg A+ (Tier 2) | |

| Raise limit | $5 million per 12 months | $75 million per 12 months |

| Investor access | Accredited and non-accredited | Accredited and non-accredited |

| Non-accredited cap | Income/net worth formula | 10% of income or net worth |

| Ongoing reporting | Annual report until conditions met | Annual, semi-annual, current reports |

| Platform requirement | Must use registered intermediary | Optional |

If you are raising under $5 million and want a faster, lower-cost path to public investors, Reg CF is the more appropriate framework. If you are raising above $5 million, or you want the credibility and investor reach that comes with a fully qualified Reg A+ offering, Tier 2 is worth the additional compliance investment.

The two are not mutually exclusive over time. Some companies run a Reg CF round at an earlier stage and return with a Reg A+ offering once they have the operating history and financial infrastructure to support it.

Related reading: The Pros and Cons of Regulation Crowdfunding

Is Reg A+ the Right Structure for Your Raise?

Reg A+ makes the most sense when three conditions are true at once: you need to raise more than $5 million, you want retail investors to participate, and you have the budget and operational capacity to manage a compliance process before, during, and after the raise.

If your target is between $5 million and $75 million, you have auditable financials, and you have an existing audience or customer base that could realistically become investors, Reg A+ deserves serious evaluation.

The ability to raise from the public at this scale, without going through a full IPO, is a structural option that did not exist for most private companies a decade ago. Most founders do not use it because they are not aware of it, not because it does not fit.

Where it does not fit: pre-revenue companies with no operating history, founders who need capital on a timeline shorter than the qualification process allows, and raises small enough that compliance overhead consumes too large a share of the proceeds.

How you structure your raise today has real consequences for who controls your company and how your cap table looks five years from now. That calculation deserves more than a surface-level comparison of raise limits.

Related reading: Equity Crowdfunding vs. Venture Capital: What Founders Actually Give Up with Each

Frequently Asked Questions

What’s the difference between Reg A and Reg A+?

Regulation A has existed since the 1930s as a small-offering exemption with a $5 million cap. Regulation A+ refers to the updated version enacted under Title IV of the JOBS Act in 2015, which raised the cap to $75 million across two tiers and made substantial changes to investor eligibility rules. When people say “Reg A+” today, they mean the current framework.

What is the maximum offering for Reg A+?

$75 million per 12-month period under Tier 2. Tier 1 is capped at $20 million per 12-month period.

Is Reg A+ a private placement?

No. A Reg A+ offering is a public offering. The securities are offered and sold to the general public, including non-accredited investors. It is exempt from full SEC registration, but it is not a private placement in the way Reg D offerings are.

Can non-US companies use Reg A+?

No. Regulation A+ is available only to companies organized and operating in the United States or Canada.

How long does a Reg A+ offering take?

From the decision to pursue Reg A+ to a qualified offering typically takes four to six months, sometimes longer depending on the complexity of the Form 1-A and the length of the SEC comment process. Planning around a 90-day timeline is not realistic. For a detailed overview of the FINRA rules governing Reg A+ offerings, the FINRA FAQ is the most current regulatory reference.

What’s the difference between Reg A+ and Reg CF?

The primary differences are raise limit ($75M vs. $5M), audit requirements, and the mandatory platform intermediary requirement that applies to Reg CF but not Reg A+. Both allow non-accredited investor participation. For a detailed comparison, see our guide to Regulation Crowdfunding.

Planet Wealth works with founders across F&B, SaaS, and energy to structure and execute compliant public raises. If you want to understand whether a Reg A+ offering fits your raise, start the conversation with our team.